Powering Progress in Southeast Asia's Renewables Development

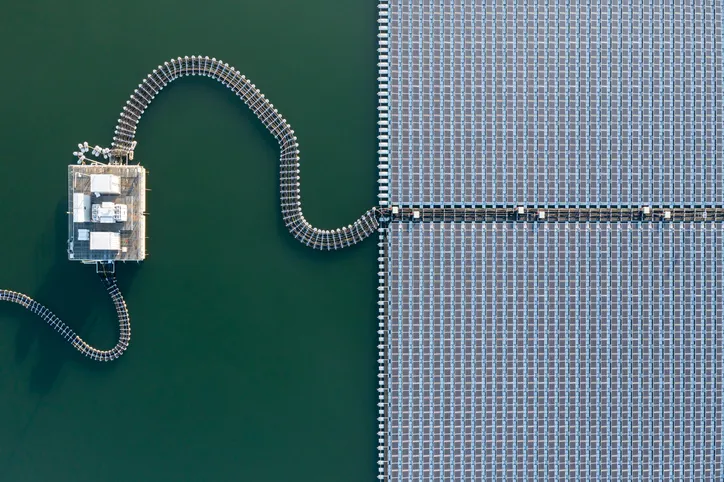

This report finds that the untapped opportunity in renewables in Southeast Asia stands at the cusp of change, as governments and corporates set high ambitions. There is a total of 17 TW of solar and wind potential in the region, which present a sizeable investment opportunity through to 2050. Aligned to net zero ambitions, governments have started setting renewables strategies, including import targets in Singapore, competitive bidding in Malaysia and power purchasing agreements in Thailand.

The current penetration of renewables, along with investment, does not yet reflect the boldness of these aspirations, as the structural environment is not as conducive to the renewables growth seen elsewhere. Net zero in the region would require accelerating yearly solar and wind capacity additions by four to six times, from 2016 to 2021 average figures, but investments are not matching this.

While these challenges exist, this report highlights early movers who have established a presence in the region, proving that success is achievable. These developers have used regulatory and local stakeholder engagement, business model innovation, such as solar-as-a-service, and technical specialisation as levers to establish market presence in Southeast Asia.

Find out more here.

McKinsey and the Singapore Economic Development Board establish the key considerations for renewables developers to succeed in Southeast Asia.

Establishing the key considerations for renewables developers to succeed in Southeast Asia.